Inflection Point Higher or Head Fake?

An Oil Market Rant: Part 2 - Update

Hope everyone is having an enjoyable summer so far. I for one am happy to see this July has been directionally much better than last year for the oil market, even if we are at much lower prices…… So, seeing as the oil market likes to keep us on our toes, I thought it would be good timing to provide a little update based on this new trend, good summer vibes, and some interesting observations from the last week. I’m beginning to suspect I must be really good at timing near term price bottoms based on when I posted my last article. Just need to work on timing the tops now….

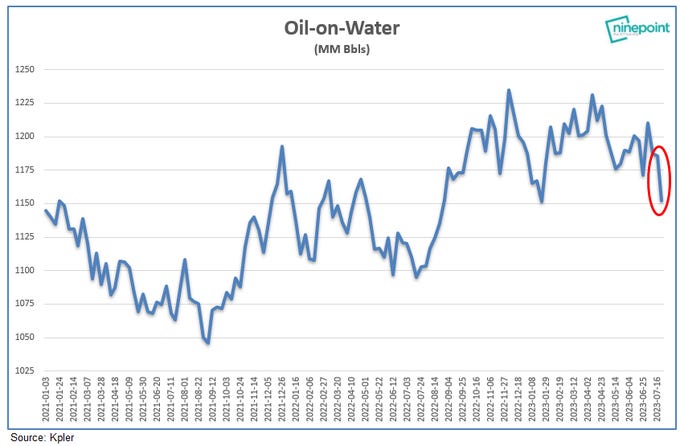

First, to follow up on the proverbial elephant in the room, the OPEC+ cuts. The belief that OPEC was suffering a crisis of confidence from the markets appears to be playing out. The market clearly remains in a “Show Me” mode, and fortunately it is seeing what it needs to see to move crude prices higher. Changes in oil-on-water for July support that OPEC+/KSA are delivering on recent mandatory and voluntary cuts.

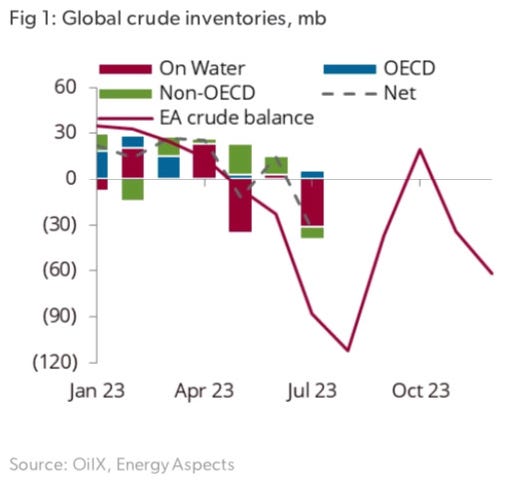

(Above) Eric Nuttal of Ninepoint Partners shows a 58 million barrel drop in in oil-on-water so far in the month of July (data source: Kpler). (Below) Energy Aspects corroborates the reduction in oil-on-water (data source: OilX) and shows the impact on global crude inventories as these reductions/continued OPEC+ production cuts begin to hit onshore inventories.

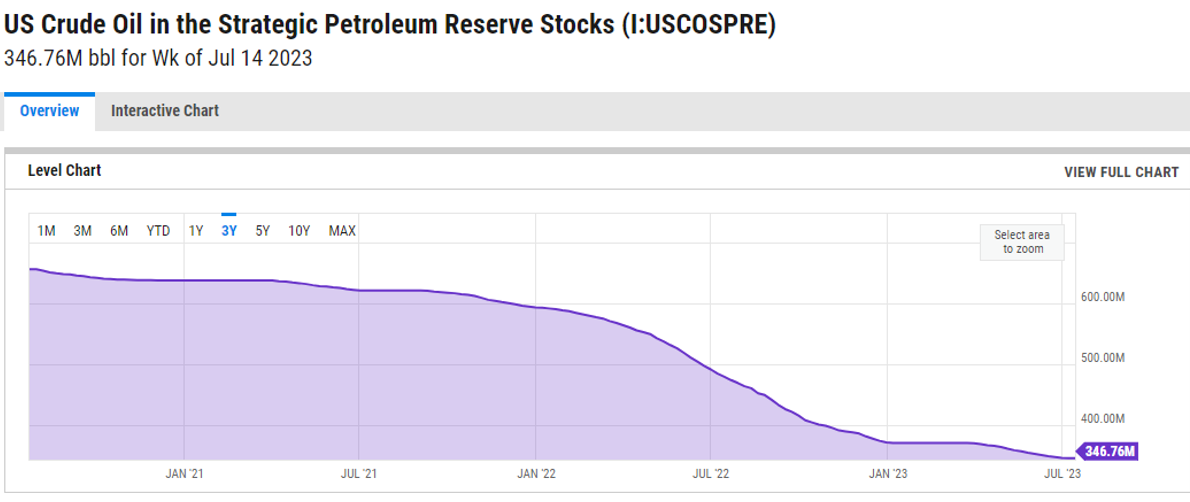

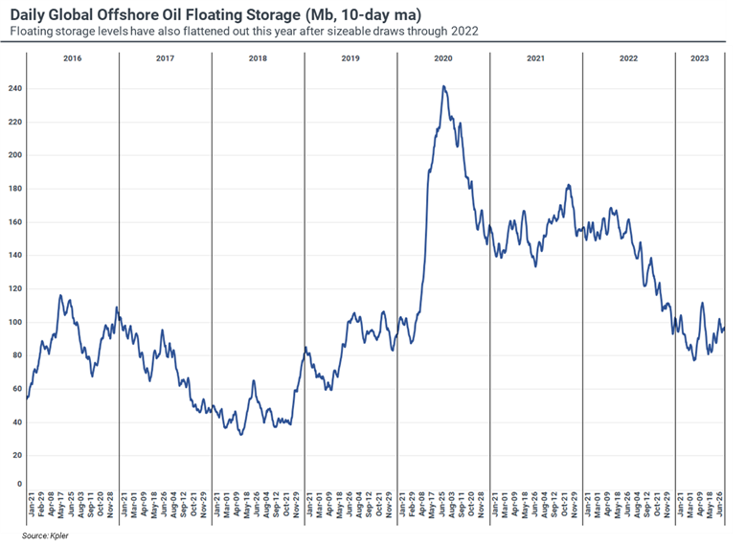

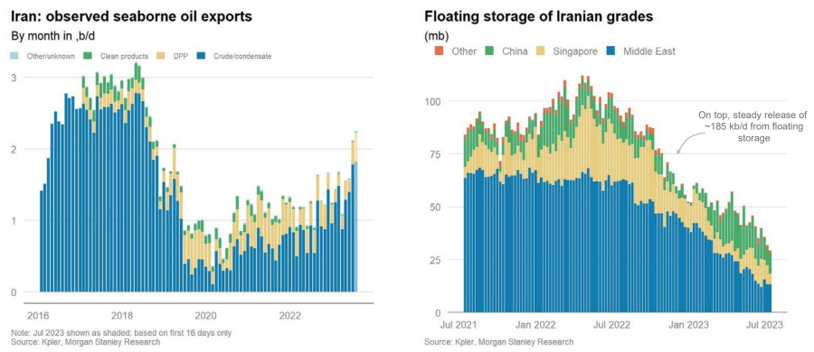

Of course, the OPEC cuts and subsequent reduction in oil-on-water being seen are not the only change to supply that hit the market. The SPR releases have ENDED and floating storage draws seem to be coming to an end as well. Since Q1 ‘21 the US SPR releases, other OECD SPR releases, and global floating storage draw downs (mostly Iranian barrels) has represented an incremental 630kbpd of supply to the market and clearly acted to support commercial inventories. From a rate of change perspective, this “supply” ending is significant in a market where the marginal barrel sets the price.

On the financial/paper market front, the move is trending as I expected with the above factors becoming more apparent to the market. (Below from my last article, published 6/28)

The culmination of the above (and many other factors) has led to a fairly extreme short positioning by managed money. This, in the context of a lower open interest/liquidity environment, ultimately could result an inflection in crude prices to much higher levels and a rapid unwinding of short positioning (short squeeze). Naturally, O&G equites would benefit from this scenario as well.

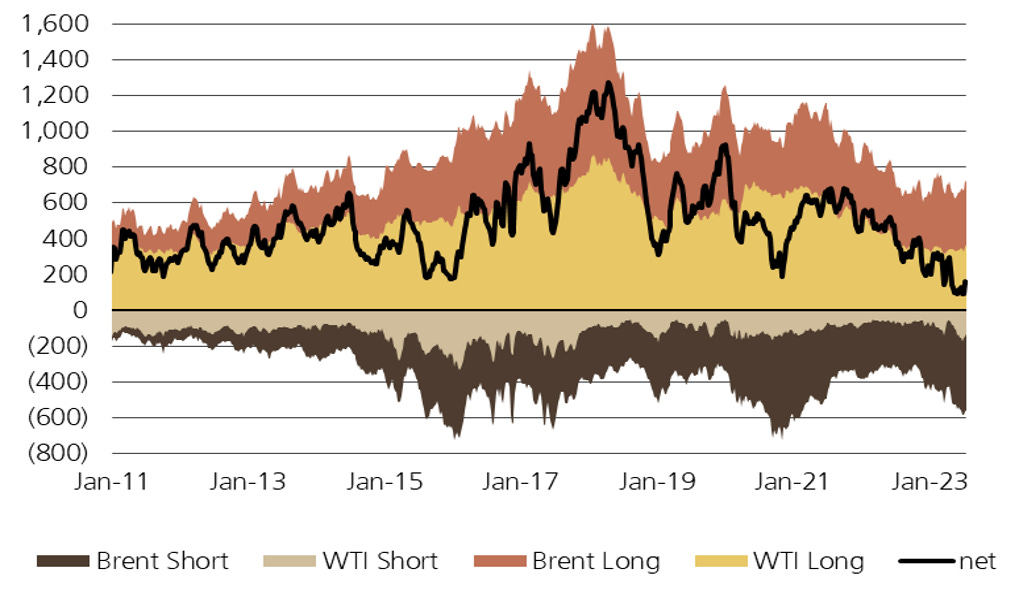

As you can see from the below chart, shorts have indeed been rapidly unwinding while longs have been adding to to their positions. WTI is up ~16% since 6/28.

That being said, the overall positioning of the market still remain extremely low from a net length and open interest perspective. (See below from Giovanni Staunovo, https://twitter.com/staunovo/status/1682477064010465282)

Interestingly, while managed money with NYMEX WTI positions have been quick to reposition, their counterparts with ICE Brent short positions have been slower to adjust. Could be quite the shock for those who hold them if these positions are left open during the extended EU summer vacation period…

Further supporting this move higher in crude prices is no head fake comes from recent moves in futures spreads, crack spreads, and product prices. Prompt Futures Spreads are now firmly in backwardation, after even Brent dipped into contango headed into July. US 3-2-1 Crack Spreads continue to inflect higher as gasoline and diesel increases outpace crudes, implying products demand is healthy. Looking into the Asian market, Singapore Gasoil Crack Spreads and Naphtha Futures continue to rally higher after bottoming in May and June, suggesting globally demand may be turning higher after an underwhelming China reopening in H1 (though seasonally, H2 does typically average +1Mbpd higher vs. H1)

The last piece of the puzzle that brings it all together is the fairly big technical signal crude gave last Friday (7/21). Crude price closing above the 200 day moving average is a trigger point many technical trader have been looking for since the breakdown last year. If it holds and we see the 50dMA cross above the 200dMA (Golden Cross), I believe we will likely see a move up to the +1 Std Dev line based on the 3 yr chart shown below.

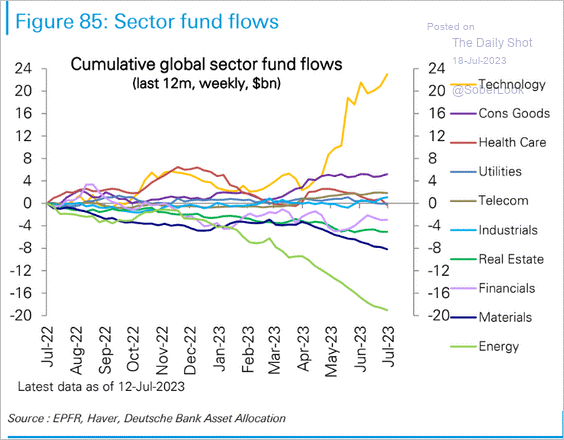

With the technical signal in place, the coming onshore inventory draws over the next several weeks should provide the fundamental basis for crude prices to move higher with money managers exiting their short positions helping the move gain momentum. However, I would hesitate to call for a +2 Std move as we will likely see some form of Chinese inventory usage (commercial/SPR) to combat prices rising higher than ~$90-$95/bbl WTI. At the same time, it seems unlikely we would get a knee jerk unwinding of any OPEC cuts (voluntary or mandated) as the group/KSA would likely take a wait and see approach with current marco economic uncertainty. This may allow for a window of stabilization in oil prices at a higher level as KSA is likely looking to over tighten and month ahead production guidance will already be set. All this sets up what could be a big move in energy equities as well. With equity flows of the past year looking like the below, I see significant upside for O&G stock over the next few months as fund flows start to adjust based on the new energy sector momentum as crude prices head higher.

Hope everyone has a good rest of the week. A hopeful cheers to crude & product draws in the EIA WPSR on Wednesday!

-RySci

*I am not a financial advisor and the above article should not be taken as investment advice. As always, DYODD

RySci’s Hot Sauce of the Week - Tia Lupita Habanero

Awesome analysis